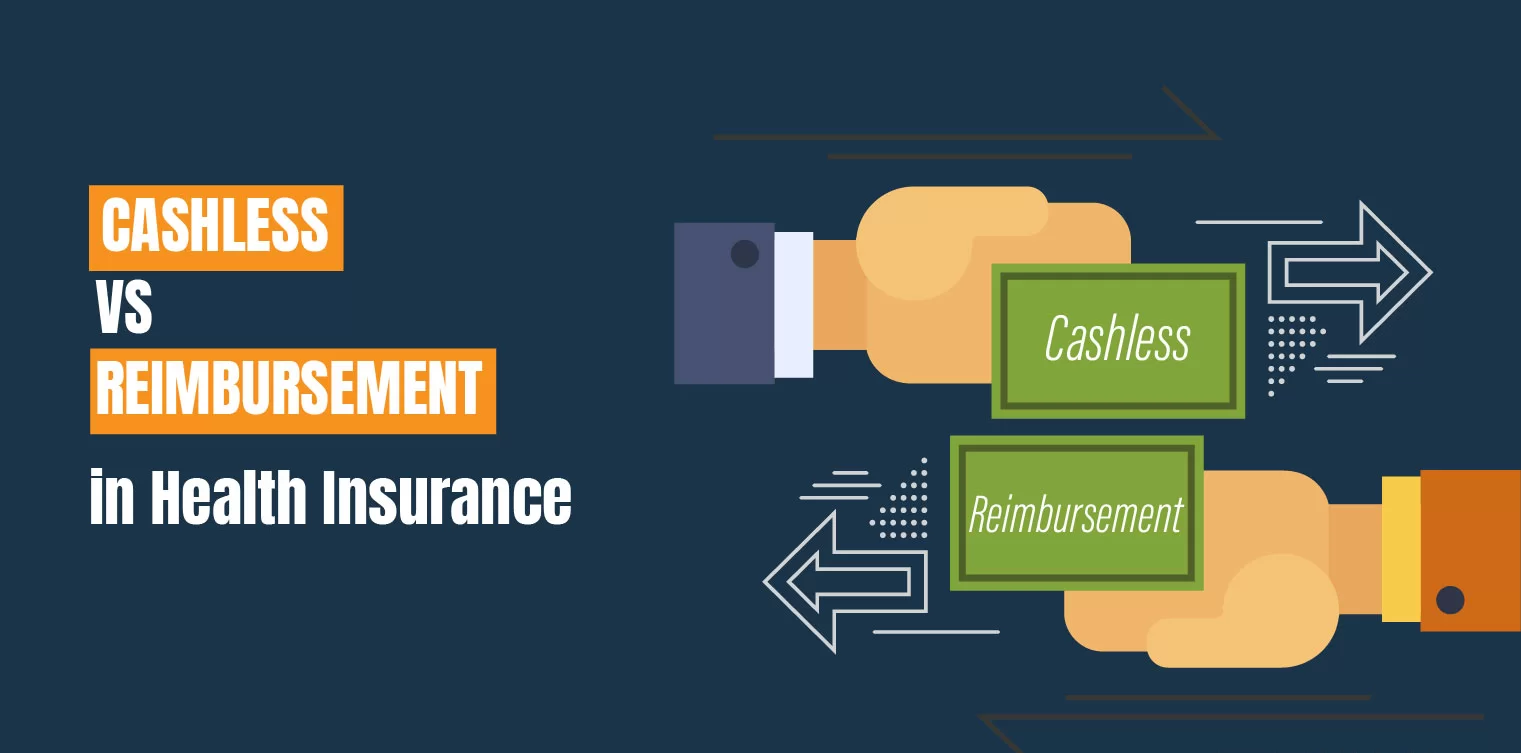

When you deal with health insurance, the two main ways to handle claims are through either cashless or reimbursement options. Both are designed to reduce your financial stress during health emergencies, but they have their own advantages and drawbacks. Your choice will hinge on factors like your habits, your proximity to network hospitals, and what suits you.

This article breaks down the specifics, perks, and best scenarios for each claim method. By the end, you’ll have enough insights to choose the right medical insurance plan for your needs.

Getting to the Basics

What Does Cashless Health Insurance Mean?

Cashless health insurance lets the insured person get treated at hospitals in the insurer’s network without paying from their own pocket during discharge. The insurance company pays the hospital bill.

To use cashless treatment:

- Go to a network hospital

- Show your health card or insurance details

- Obtain approval from the insurer

- Receive care without upfront payment (except for excluded items)

What Does Reimbursement Mean in Health Insurance?

In a reimbursement model, the policyholder covers hospital expenses first and later requests repayment from the insurer. After discharge, they must submit all bills, prescriptions, forms, and the discharge summary. The insurer then repays the amount based on the policy rules.

Main Differences Between Reimbursement and Cashless

Here are the key differences between reimbursement and cashless health insurance:

| Feature | Cashless | Reimbursement |

| Hospital Network | Works with network or empanelled hospitals | Covers treatment at any hospital, networked or not |

| Upfront Payment | Not needed, except for uncovered costs | Needs to be paid by the policyholder upfront |

| Claim Process Time | Speeds up with advance authorisation | Can take from a few days to several weeks after discharge |

| Paperwork | Requires very little paperwork | Involves a lot of documentation and needs all original records |

| Emergency Suitability | Works well in emergencies | Less ideal because of the need to pay upfront |

Advantages and Disadvantages of Both Options

Advantages of Cashless Claims

- No money worries during or after the hospital stay

- Approval comes for most scheduled procedures

- Reduces hassle with minimal documentation

Disadvantages of Cashless Claims

- You must rely on network hospitals

- During emergencies, pre-authorisation can delay prompt treatment

Advantages of Reimbursement Claims

- You can pick any hospital, even those outside the network.

- These work well in areas where network hospitals aren’t around.

Disadvantages of Reimbursement Claims

- You have to pay first, which might be tough in urgent situations.

- The process takes longer and needs a lot of paperwork.

Which Option Works Best?

There’s no universal answer. Think about your situation:

- Living in a city with access to good network hospitals? Go for a cashless option.

- Do you travel often or live far away? A reimbursement option can offer better flexibility.

- Need immediate help during emergencies? Cashless works best.

- Need specific care at hospitals outside the network? Reimbursement might be your only choice.

When picking a medical insurance plan, aim for one that includes both options. It can be helpful during tough moments.

How to Get the Best from Your Health Insurance

Here’s how to make the most of your health insurance:

- Check Out Network Hospitals: Learn which nearby hospitals allow cashless claims through your insurer.

- Keep All Important Papers Ready: Always keep medical records, ID proof, and your policy card in one place. You’ll need them whether making a cashless claim or seeking reimbursement.

- Notify Your Insurer Quickly: Let your insurance company know about the claim within the required time. This is within 24 hours for emergencies or between 48 to 72 hours for planned cases.

- Understand Sub-Limits and Co-Pay Details: Be sure you are aware of room rent caps, disease-specific expense limits, and co-pay percentages in your health policy.

Conclusion

Knowing the distinction between cashless and reimbursement health insurance claims helps you manage medical costs better. Cashless claims provide ease and quick relief, while reimbursement claims allow access to more treatment options.

No matter which option you choose, make sure your health insurance plan covers everything you need, is easy to understand, and matches your healthcare requirements.

Chola MS Health Insurance provides cashless options and reimbursements through a vast network of hospitals in India. Chola MS has earned the trust of many Indian families by focusing on making claims simple and providing plans customised to their needs.

FAQs

Q1: Can I use a cashless facility at any hospital?

No, you can use cashless claims at hospitals included in your insurer’s network. Make sure to check their updated list of network hospitals.

Q2: How much time does it take to process a health insurance claim reimbursement?

Reimbursement takes 7 to 30 working days once you submit all the documents. Missing paperwork or extra information requirements can delay the process.

Q3: What if I get treated at a hospital outside the network?

You can file for reimbursement by providing your medical and billing paperwork. It will depend on your policy’s coverage and terms.

Q4: Are all types of treatments included under both cashless and reimbursement claims?

Policy terms decide which treatments qualify. Exclusions usually apply to procedures like cosmetic surgeries, dental care, or alternative treatments.

Q5: Can I use cashless benefits and claim the remaining through reimbursement?

It is possible in some cases. When specific costs are not paid for under cashless, you might pay upfront and then file reimbursement, if allowed.